And that being said, let's start.

I. The only thing you have to change to make the bot work (insert your private keys).

II. Things you don't need to change, but might to easily make the bot better (changing the strategy, parameters, etc.).

III. Things you don't need to change, but might if you want to make more advanced changes to the bot.

* '>' here represents the crossing over

* '<' here represents the crossing under

To start working with this notebook, you need Python and Jupyter Notebook.

To get Python, go to https://www.anaconda.com, download it, and install it.

After you install Anaconda on your computer, create a new environment in it (with 1 click) and install Jupyter Notebook and CMD.exe Prompt within the environment (with 2 clicks).

To use the bot you also need, at least, a free account at Alpaca. To get that account go to https://alpaca.markets and sign up to it. At the moment, if you only want to use paper trading account, you only need an email address to sign up.

After you do it, you are ready to start working with this notebook.

These 2 lines of code are the only two lines you have to change to make the bot work. You need to put here your own keys to Alpaca account. At the moment of creating this tutorial, Alpaca is free to use for everyone and with paper account you only need an email address to sign up.

#SuperAI Trading Bot - 1. mandatory cell to run

KEY_ID = "your own KEY_ID" #replace it with your own KEY_ID from Alpaca: https://alpaca.markets/

SECRET_KEY = "your own SECRET_KEY" #replace it with your own SECRET_KEY from Alpaca

At first, we install all the necessary libraries and packages.

You may install more of them if you need, but the ones you find here are enough to run the bot.

You can skip it if you already have them installed or you can upgrade or downgrade them if necessary.

#SuperAI Trading Bot - optional cell

#You need to run it only once when you create new environment

#install and upgrade TA-Lib library

#1. On Windows and if you are using Anaconda,

#open Anaconda Prompt and

#write in Anaconda Prompt: conda install -c conda-forge ta-lib

#2. If it doesn't work or if you work on Linux or Mac you may unahsh pip line and check this way

#!pip install TA-Lib --upgrade

#3. You could also check this site to learn how else you could do install it

#https://pypi.org/project/TA-Lib/

#SuperAI Trading Bot - optional cell

#You need to run it only once when you create new environment

#install and upgrade all the libraries, packages, and modules which you don't have

!pip install alpaca-trade-api --upgrade

#https://pypi.org/project/alpaca-trade-api/

!pip install numpy==1.22.4

#https://pypi.org/project/numpy/

!pip install pandas --upgrade

#https://pypi.org/project/pandas/

!pip install ta --upgrade

#https://pypi.org/project/ta/

!pip install vectorbt --upgrade

#https://pypi.org/project/vectorbt/

!pip install yfinance --upgrade

#https://pypi.org/project/yfinance/

#SuperAI Trading Bot - 2. mandatory cell to run

#import all you need

import alpaca_trade_api as tradeapi

from alpaca_trade_api.rest import TimeFrame

import datetime

from datetime import timedelta

import math

import numpy as np

import pandas as pd

import sys

import ta

import talib as ta_lib

import time

import vectorbt as vbt

import warnings

warnings.filterwarnings('ignore')

print("Python version: {}".format(sys.version))

print("alpaca trade api version: {}".format(tradeapi.__version__))

print("numpy version: {}".format(np.__version__))

print("pandas version: {}".format(pd.__version__))

print("ta_lib version: {}".format(ta_lib.__version__))

print("vectorbt version: {}".format(vbt.__version__))

Check the version of TA library

pip show ta

You can choose any asset that can be traded with Alpaca API and paste the ticker of the asset in here.

#SuperAI Trading Bot - 3. mandatory cell to run

(asset, asset_type, rounding) = ("BTCUSD", "crypto", 0)

#if you want to trade crypto check: https://alpaca.markets/support/what-cryptocurrencies-does-alpaca-currently-support/

#rounding declares the no of numbers after comma for orders

#read more about minimum qty and qty increment at https://alpaca.markets/docs/trading/crypto-trading/

#(asset, asset_type, data_source) = ("AAPL", "stock", "Yahoo") #("AAPL", "stock", "Alpaca")

#if you want to trade stocks replace it with the ticker of the company you prefer: https://www.nyse.com/listings_directory/stock

#you can also use "Alpaca" as a data_source

#Alpaca gives you free access to more historical data, but in a free plan doesn't allow you to access data from last 15 minutes

#Yahoo gives you access to data from last 15 minutes, but gives you only 7 days of historical data with 1-min interval at a time

#from last month

Here you can declare which technical indicators and candlestick patterns you want to use as signals to buy and sell stocks and how the signals should be created (what should the logic for buying and selling be).

You have 6 indicators from 4 categories to use:

You have 8 candlestick patterns from 3 categories to use:

1st Sample Strategy - with moving average: BUY when CLOSE PRICE crosses over MA ==> SELL when CLOSE PRICE crosses under MA

#SuperAI Trading Bot - 4. mandatory cell to run

# 1st SAMPLE STRATEGY - WITH MOVING AVERAGE

# BUY WHEN CLOSE PRICE CROSSES OVER THE MOVING AVERAGE

# SELL WHEN CLOSE PRICE CROSSES UNDER THE MOVING AVERAGE

def create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime, #Time to abstain from buying and forced selling

ma, ma_fast, ma_slow, #Moving Average

macd, macd_diff, macd_sign, #Moving Average Convergence Divergence

rsi, rsi_entry, rsi_exit, #Relative Strength Index

stoch, stoch_signal, stoch_entry, stoch_exit, #Stochastic

bb_low, bb_high, #Bollinger Bands

mfi, mfi_entry, mfi_exit, #Money Flow Index

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3, #Candle signals to buy

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3, #Candle signals to sell

candle_buy_sell_signal_1, candle_buy_sell_signal_2): #Candle signals to buy or sell

SuperAI_signal_buy = np.where(

(buylesstime != 1)

&

((close_prices > ma) & (shifted(close_prices, 1) <= shifted(ma, 1)))

, 1, 0) #1 is buy, -1 is sell, 0 is do nothing

SuperAI_signal = np.where(

(selltime == 1)

|

((close_prices < ma) & (shifted(close_prices, 1) >= shifted(ma, 1)))

, -1, SuperAI_signal_buy) #1 is buy, -1 is sell, 0 is do nothing

global cs_name

cs_name = '1st Sample Strategy'

return SuperAI_signal

#SuperAI Trading Bot - 5. mandatory cell to run

# PARAMETERS FOR CONNECTING TO ALPACA

#The URLs we use here are for paper trading. If you want to use your bot with your live account, you should change these URLs to

#those dedicated to live account at Alpaca. Just remember, that with live account you are using real money,

#so be sure that your bot works as you want it to work. Test your bot before you give it real money to trade.

APCA_API_BASE_URL = "https://paper-api.alpaca.markets"

#Connecting to API

api = tradeapi.REST(KEY_ID, SECRET_KEY, APCA_API_BASE_URL, "v2")

#Keys to use Alpaca with vectorbt backtesting library

vbt.settings.data['alpaca']['key_id'] = KEY_ID

vbt.settings.data['alpaca']['secret_key'] = SECRET_KEY

# PARAMETERS USED BY SUPERAI TRADING BOT WITH AND WITHOUT OPTIMIZATION

funds_percentage = 90 #replace it with the percentage of the amount of money you have to use for trading

take_profit_percent = 0.5 # 50%

stop_loss_percent = 0.05 # 5%

#Parameters for live trading (during paper trading take profit and stop loss are always on, but you can change it in the code)

take_profit_automatically = True #change to False if you don't want to use take_profit function during live trading

stop_loss_automatically = True #change to False if you don't want to use stop_loss function during live trading

#Funds to invest

account = api.get_account()

cash = float(account.cash)

buying_power = float(account.buying_power)

funds = cash * funds_percentage / 100

#Parameters for downloading the data

data_timeframe = '1m' #replace with preferable time between data: 1m, 5m, 15m, 30m, 1h, 1d

data_limit = None #replace with the limit of the data to download to speed up the process (500, 1000, None)

crypto_data_timeframe = TimeFrame.Minute

preferred_exchange = "CBSE"

#Basic parameters to use for indicators before/without optimization

ma_window_max = ma_window = ma_timeframe = 28

ma_fast_window_max = ma_fast_window = ma_fast_timeframe = 14

ma_slow_window_max = ma_slow_window = ma_slow_timeframe = 50

macd_slow_window_max = macd_slow_window = macd_slow_timeframe = 26

macd_fast_window_max = macd_fast_window = macd_fast_timeframe = 12

macd_sign_window_max = macd_sign_window = macd_signal_timeframe = 9

rsi_window_max = rsi_window = rsi_timeframe = 14

rsi_entry_max = rsi_entry = rsi_oversold_threshold = 30

rsi_exit_max = rsi_exit = rsi_overbought_threshold = 70

stoch_window_max = stoch_window = stoch_timeframe = 14

stoch_smooth_window_max = stoch_smooth_window = stoch_smooth_timeframe = 3

stoch_entry_max = stoch_entry = stoch_oversold_threshold = 20

stoch_exit_max = stoch_exit = stoch_overbought_threshold = 80

bb_window_max = bb_window = bb_timeframe = 10

bb_dev_max = bb_dev = bb_dev = 2

mfi_window_max = mfi_window = mfi_timeframe = 14

mfi_entry_max = mfi_entry = mfi_oversold_threshold = 20

mfi_exit_max = mfi_exit = mfi_overbought_threshold = 80

#Parameters to optimize during backtesting

ma_window_opt = np.arange(14, 30, step=14, dtype=int) #[14, 28]

ma_fast_window_opt = np.arange(14, 22, step=7, dtype=int) #[14, 21]

ma_slow_window_opt = np.arange(30, 51, step=20, dtype=int) #[30, 50]

macd_slow_window_opt = np.arange(26, 27, step=100, dtype=int) #[26]

macd_fast_window_opt = np.arange(12, 13, step=100, dtype=int) #[12]

macd_sign_window_opt = np.arange(9, 10, step=100, dtype=int) #[9]

rsi_window_opt = np.arange(14, 22, step=7, dtype=int) #[14, 21]

rsi_entry_opt = np.arange(20, 31, step=10, dtype=int) #[20, 30]

rsi_exit_opt = np.arange(70, 81, step=10, dtype=int) #[70, 80]

stoch_window_opt = np.arange(14, 15, step=100, dtype=int) #[14]

stoch_smooth_window_opt = np.arange(3, 4, step=100, dtype=int) #[3]

stoch_entry_opt = np.arange(20, 21, step=100, dtype=int) #[20]

stoch_exit_opt = np.arange(80, 81, step=100, dtype=int) #[80]

bb_window_opt = np.arange(10, 21, step=10, dtype=int) #[10, 20]

bb_dev_opt = np.arange(2, 3, step=100, dtype=int) #[2]

mfi_window_opt = np.arange(14, 22, step=7, dtype=int) #[14, 21]

mfi_entry_opt = np.arange(10, 21, step=10, dtype=int) #[10, 20]

mfi_exit_opt = np.arange(80, 91, step=10, dtype=int) #[80, 90]

# PARAMETERS FOR DECISIONS REGARDING OPTIONS AND TIME OF BACKTESTING AND LIVE TRADING

optimization = True #True or False

validation = True #True or False

#Dates to download data for backtesting training phase

data_start = '2022-07-01' #replace with the starting point for collecting data

data_end = '2022-07-31' #replace with the ending point for collecting the data

#Dates to download data for backtesting validation phase

valid_start = '2022-08-01'

valid_end = '2022-08-15'

#The function for declaring trading hours

def trading_buy_sell_time():

if asset_type == 'stock':

#more about trading hours at: https://alpaca.markets/docs/trading/orders/#extended-hours-trading

trading_hour_start = "09:30"

trading_hour_stop = "16:00"

#time when you don't want to buy at the beginning of the day

buyless_time_start_1 = "09:30"

buyless_time_end_1 = "09:45"

buyless_time_start_2 = "15:55"

buyless_time_end_2 = "16:00"

#time when you want to sell by the end of the day

selltime_start = "15:55"

selltime_end = "16:00"

elif asset_type == 'crypto':

trading_hour_start = "00:00"

trading_hour_stop = "23:59"

#time when you don't want to buy at the beginning of the day

buyless_time_start_1 = "23:59"

buyless_time_end_1 = "00:01"

buyless_time_start_2 = "23:58"

buyless_time_end_2 = "23:59"

#time when you want to sell by the end of the day

selltime_start = "23:59"

selltime_end = "00:00"

return (trading_hour_start, trading_hour_stop,

buyless_time_start_1, buyless_time_end_1, buyless_time_start_2, buyless_time_end_2,

selltime_start, selltime_end)

#DataFrame for testing various strategies

columns = ('Strategy', 'Basic Returns', 'Returns After Optimization', 'Returns From Validation')

strategies = pd.DataFrame([], columns=columns).set_index('Strategy')

strategy_returns = ['0',0,0,0]

#SuperAI Trading Bot - 6. mandatory cell to run

# 1. ALL THE OTHER NECESSARY FUNCTIONS AND VARIABLES OF THE BOT USED DURING BACKTESTING

#helper function to shift data in order to test differences between data from x min and data from x-time min

def shifted(data, shift_window):

data_shifted = np.roll(data, shift_window)

if shift_window >= 0:

data_shifted[:shift_window] = np.NaN

elif shift_window < 0:

data_shifted[shift_window:] = np.NaN

return data_shifted

#preparing data in one function

def prepare_data(start_date, end_date):

data_start = start_date

data_end = end_date

if asset_type == "stock" and data_source == "Alpaca":

full_data = vbt.AlpacaData.download(asset, start=data_start, end=data_end,

timeframe=data_timeframe, limit=data_limit).get()

elif asset_type == "stock" and data_source == "Yahoo":

try:

full_data = vbt.YFData.download(asset, start = data_start, end= data_end,

interval=data_timeframe).get().drop(["Dividends", "Stock Splits"], axis=1)

except:

full_data = vbt.AlpacaData.download(asset, start=data_start, end=data_end,

timeframe=data_timeframe, limit=data_limit).get()

print("""\nI tried downloading data with Yahoo, but something went wrong so I downloaded data with Alpaca.

That means than the data might not look the same as the data from Yahoo.\n\n""")

elif asset_type == "crypto":

crypto_data = api.get_crypto_bars(asset, crypto_data_timeframe, start = data_start, end=data_end).df

full_crypto_data = crypto_data[crypto_data['exchange'] == preferred_exchange]

full_data = full_crypto_data.rename(str.capitalize, axis=1).drop(["Exchange", "Trade_count", "Vwap"], axis=1)

else:

print("You have to declare asset type as crypto or stock for me to work properly.")

full_data.index = full_data.index.tz_convert('America/New_York')

(trading_hour_start, trading_hour_stop,

buyless_time_start_1, buyless_time_end_1, buyless_time_start_2, buyless_time_end_2,

selltime_start, selltime_end) = trading_buy_sell_time()

data = full_data.copy()

data = data.between_time(trading_hour_start, trading_hour_stop)

not_time_to_buy_1 = data.index.indexer_between_time(buyless_time_start_1, buyless_time_end_1)

not_time_to_buy_2 = data.index.indexer_between_time(buyless_time_start_2, buyless_time_end_2)

not_time_to_buy = np.concatenate((not_time_to_buy_1, not_time_to_buy_2), axis=0)

not_time_to_buy = np.unique(not_time_to_buy)

data["NotTimeToBuy"] = 1

data["BuylessTime"] = data.iloc[not_time_to_buy, 5]

data["BuylessTime"] = np.where(np.isnan(data["BuylessTime"]), 0, data["BuylessTime"])

data = data.drop(["NotTimeToBuy"], axis=1)

time_to_sell = data.index.indexer_between_time(selltime_start, selltime_end)

data["TimeToSell"] = 1

data["SellTime"] = data.iloc[time_to_sell, 6]

data["SellTime"] = np.where(np.isnan(data["SellTime"]), 0, data["SellTime"])

data = data.drop(["TimeToSell"], axis=1)

open_prices = data["Open"]

high_prices = data["High"]

low_prices = data["Low"]

close_prices = data["Close"]

volume = data["Volume"]

buylesstime = data["BuylessTime"]

selltime = data["SellTime"]

return open_prices, high_prices, low_prices, close_prices, volume, buylesstime, selltime

def starting_max_parameters():

#assigning the starting parameters as previously declared

global ma_window_max, ma_fast_window_max, ma_slow_window_max

global macd_slow_window_max, macd_fast_window_max, macd_sign_window_max

global rsi_window_max, rsi_entry_max, rsi_exit_max

global stoch_window_max, stoch_smooth_window_max, stoch_entry_max, stoch_exit_max

global bb_window_max, bb_dev_max, mfi_window_max

global mfi_entry_max, mfi_exit_max

ma_window_max = ma_window

ma_fast_window_max = ma_fast_window

ma_slow_window_max = ma_slow_window

macd_slow_window_max = macd_slow_window

macd_fast_window_max = macd_fast_window

macd_sign_window_max = macd_sign_window

rsi_window_max = rsi_window

rsi_entry_max = rsi_entry

rsi_exit_max = rsi_exit

stoch_window_max = stoch_window

stoch_smooth_window_max = stoch_smooth_window

stoch_entry_max = stoch_entry

stoch_exit_max = stoch_exit

bb_window_max = bb_window

bb_dev_max = bb_dev

mfi_window_max = mfi_window

mfi_entry_max = mfi_entry

mfi_exit_max = mfi_exit

# Custom SuperAI Indicator

# Signals Function

def superai_signals (open_prices, high_prices, low_prices, close_prices, volume, buylesstime, selltime,

ma_window = ma_timeframe,

ma_fast_window = ma_fast_timeframe,

ma_slow_window = ma_slow_timeframe,

macd_slow_window = macd_slow_timeframe,

macd_fast_window = macd_fast_timeframe,

macd_sign_window = macd_signal_timeframe,

rsi_window = rsi_timeframe,

rsi_entry = rsi_oversold_threshold,

rsi_exit = rsi_overbought_threshold,

stoch_window = stoch_timeframe,

stoch_smooth_window = stoch_smooth_timeframe,

stoch_entry = stoch_oversold_threshold,

stoch_exit = stoch_overbought_threshold,

bb_window = bb_timeframe,

bb_dev = bb_dev,

mfi_window = mfi_timeframe,

mfi_entry = mfi_oversold_threshold,

mfi_exit = mfi_overbought_threshold):

rsi = vbt.IndicatorFactory.from_ta('RSIIndicator').run(close_prices, window = rsi_window).rsi.to_numpy()

stoch = vbt.IndicatorFactory.from_ta('StochasticOscillator').run(

high_prices, low_prices, close_prices, window = stoch_window, smooth_window = stoch_smooth_window).stoch.to_numpy()

stoch_signal = vbt.IndicatorFactory.from_ta('StochasticOscillator').run(

high_prices, low_prices, close_prices, window = stoch_window,

smooth_window = stoch_smooth_window).stoch_signal.to_numpy()

ma = vbt.IndicatorFactory.from_ta('EMAIndicator').run(close_prices, window = ma_window).ema_indicator.to_numpy()

ma_fast = vbt.IndicatorFactory.from_ta('EMAIndicator').run(close_prices, window = ma_fast_window).ema_indicator.to_numpy()

ma_slow = vbt.IndicatorFactory.from_ta('EMAIndicator').run(close_prices, window = ma_slow_window).ema_indicator.to_numpy()

macd = vbt.IndicatorFactory.from_ta('MACD').run(

close_prices, window_slow = macd_slow_window, window_fast = macd_fast_window,

window_sign = macd_sign_window).macd.to_numpy()

macd_diff = vbt.IndicatorFactory.from_ta('MACD').run(

close_prices, macd_slow_window, window_fast = macd_fast_window,

window_sign = macd_sign_window).macd_diff.to_numpy()

macd_sign = vbt.IndicatorFactory.from_ta('MACD').run(

close_prices, macd_slow_window, window_fast = macd_fast_window,

window_sign = macd_sign_window).macd_signal.to_numpy()

bb_low = vbt.IndicatorFactory.from_ta('BollingerBands').run(

close_prices, window = bb_window, window_dev = bb_dev).bollinger_lband.to_numpy()

bb_high = vbt.IndicatorFactory.from_ta('BollingerBands').run(

close_prices, window = bb_window, window_dev = bb_dev).bollinger_hband.to_numpy()

mfi = vbt.IndicatorFactory.from_ta('MFIIndicator').run(

high_prices, low_prices, close_prices, volume, window = mfi_timeframe).money_flow_index.to_numpy()

candle_buy_signal_1 = vbt.IndicatorFactory.from_talib('CDLHAMMER').run(

open_prices, high_prices, low_prices, close_prices).integer.to_numpy() # 'Hammer'

candle_buy_signal_2 = vbt.IndicatorFactory.from_talib('CDLMORNINGSTAR').run(

open_prices, high_prices, low_prices, close_prices).integer.to_numpy() # 'Morning star'

candle_buy_signal_3 = vbt.IndicatorFactory.from_talib('CDL3WHITESOLDIERS').run(

open_prices, high_prices, low_prices, close_prices).integer.to_numpy() # 'Three White Soldiers'

candle_sell_signal_1 = vbt.IndicatorFactory.from_talib('CDLSHOOTINGSTAR').run(

open_prices, high_prices, low_prices, close_prices).integer.to_numpy() # 'Shooting star'

candle_sell_signal_2 = vbt.IndicatorFactory.from_talib('CDLEVENINGSTAR').run(

open_prices, high_prices, low_prices, close_prices).integer.to_numpy() # 'Evening star'

candle_sell_signal_3 = vbt.IndicatorFactory.from_talib('CDL3BLACKCROWS').run(

open_prices, high_prices, low_prices, close_prices).integer.to_numpy() # '3 Black Crows'

candle_buy_sell_signal_1 = vbt.IndicatorFactory.from_talib('CDLENGULFING').run(

open_prices, high_prices, low_prices, close_prices).integer.to_numpy() # 'Engulfing: Bullish (buy) / Bearish (sell)'

candle_buy_sell_signal_2 = vbt.IndicatorFactory.from_talib('CDL3OUTSIDE').run(

open_prices, high_prices, low_prices, close_prices).integer.to_numpy() # 'Three Outside: Up (buy) / Down (sell)'

SuperAI_signal = create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime,

ma, ma_fast, ma_slow,

macd, macd_diff, macd_sign,

rsi, rsi_entry, rsi_exit,

stoch, stoch_signal, stoch_entry, stoch_exit,

bb_low, bb_high,

mfi, mfi_entry, mfi_exit,

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3,

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3,

candle_buy_sell_signal_1, candle_buy_sell_signal_2)

return SuperAI_signal

#Parameters to optimize

parameters_names = ["ma_window", "ma_fast_window", "ma_slow_window",

"macd_slow_window", "macd_fast_window", "macd_sign_window",

"rsi_window", "rsi_entry", "rsi_exit",

"stoch_window", "stoch_smooth_window", "stoch_entry", "stoch_exit",

"bb_window", "bb_dev",

"mfi_window", "mfi_entry", "mfi_exit"]

#Indicator

SuperAI_Ind = vbt.IndicatorFactory(

class_name = "SuperAI_Ind",

short_name = "SuperInd",

input_names = ["open", "high", "low", "close", "volume", "buylesstime", "selltime"],

param_names = parameters_names,

output_names = ["output"]).from_apply_func(superai_signals,

ma_window = ma_timeframe,

ma_fast_window = ma_fast_timeframe,

ma_slow_window = ma_slow_timeframe,

macd_slow_window = macd_slow_timeframe,

macd_fast_window = macd_fast_timeframe,

macd_sign_window = macd_signal_timeframe,

rsi_window = rsi_timeframe,

rsi_entry = rsi_oversold_threshold,

rsi_exit = rsi_overbought_threshold,

stoch_window = stoch_timeframe,

stoch_smooth_window = stoch_smooth_timeframe,

stoch_entry = stoch_oversold_threshold,

stoch_exit = stoch_overbought_threshold,

bb_window = bb_timeframe,

bb_dev = bb_dev,

mfi_window = mfi_timeframe,

mfi_entry = mfi_oversold_threshold,

mfi_exit = mfi_overbought_threshold)

def SuperAI_Backtester():

#BACKTESTING WITH TRAINING AND VALIDATION SET

print("\nI start the backtesting. The declared parameters at the moment are:\n")

#Resetting the parameters to the declared ones

starting_max_parameters()

global ma_window_max, ma_fast_window_max, ma_slow_window_max

global macd_slow_window_max, macd_fast_window_max, macd_sign_window_max

global rsi_window_max, rsi_entry_max, rsi_exit_max

global stoch_window_max, stoch_smooth_window_max, stoch_entry_max, stoch_exit_max

global bb_window_max, bb_dev_max, mfi_window_max

global mfi_entry_max, mfi_exit_max

basic_returns = np.NaN

optimized_returns = np.NaN

validated_returns = np.NaN

print(""" ma_window_max: {}, ma_fast_window_max: {}, ma_slow_window_max: {},

macd_slow_window_max: {}, macd_fast_window_max: {}, macd_sign_window_max: {},

rsi_window_max: {}, rsi_entry_max: {}, rsi_exit_max: {},

stoch_window_max: {}, stoch_smooth_window_max: {}, stoch_entry_max: {}, stoch_exit_max: {},

bb_window_max: {}, bb_dev_max: {},

mfi_window_max: {}, mfi_entry_max: {}, mfi_exit_max: {}\n""".format(

ma_window_max, ma_fast_window_max, ma_slow_window_max,

macd_slow_window_max, macd_fast_window_max, macd_sign_window_max,

rsi_window_max, rsi_entry_max, rsi_exit_max,

stoch_window_max, stoch_smooth_window_max, stoch_entry_max, stoch_exit_max,

bb_window_max, bb_dev_max, mfi_window_max,

mfi_entry_max, mfi_exit_max))

print("\nI'm downloading the data for {} from {} to {}.\n".format(asset, data_start, data_end))

#Remembering the backtested asset

global backtested_asset

backtested_asset = asset

#Preparing data

open_prices, high_prices, low_prices, close_prices, volume, buylesstime, selltime = prepare_data(data_start, data_end)

print("I have the data. I start doing the calculations.\n")

#TESTING THE PROTOTYPE

trading_signals = SuperAI_Ind.run(open_prices, high_prices, low_prices, close_prices, volume, buylesstime, selltime,

ma_window = ma_timeframe,

ma_fast_window = ma_fast_timeframe,

ma_slow_window = ma_slow_timeframe,

macd_slow_window = macd_slow_timeframe,

macd_fast_window = macd_fast_timeframe,

macd_sign_window = macd_signal_timeframe,

rsi_window = rsi_timeframe,

rsi_entry = rsi_oversold_threshold,

rsi_exit= rsi_overbought_threshold,

stoch_window = stoch_timeframe,

stoch_smooth_window = stoch_smooth_timeframe,

stoch_entry = stoch_oversold_threshold,

stoch_exit = stoch_overbought_threshold,

bb_window = bb_timeframe,

bb_dev = bb_dev,

mfi_window = mfi_timeframe,

mfi_entry = mfi_oversold_threshold,

mfi_exit= mfi_overbought_threshold,

param_product = True)

entries = trading_signals.output == 1.0

exits = trading_signals.output == -1.0

SuperAI_portfolio = vbt.Portfolio.from_signals(close_prices,

entries,

exits,

init_cash = 100000,

tp_stop = take_profit_percent,

sl_stop = stop_loss_percent,

fees = 0.00)

returns = SuperAI_portfolio.total_return() * 100

basic_returns = returns

stats = SuperAI_portfolio.stats()

print("I did the backtest with previously declared indicators and parameters.\n")

print("Returns before optimization: ", returns, "\n")

print("Stats before optimization:")

print(stats, "\n")

#OPTIMIZING THE BOT WITH A GRID OF DIFFERENT POSSIBILITIES FOR PREFERRED PARAMETER

if optimization == True:

print("I start the optimization. The parameters before optimization are:\n")

print(""" ma_window_max: {}, ma_fast_window_max: {}, ma_slow_window_max: {},

macd_slow_window_max: {}, macd_fast_window_max: {}, macd_sign_window_max: {},

rsi_window_max: {}, rsi_entry_max: {}, rsi_exit_max: {},

stoch_window_max: {}, stoch_smooth_window_max: {}, stoch_entry_max: {}, stoch_exit_max: {},

bb_window_max: {}, bb_dev_max: {},

mfi_window_max: {}, mfi_entry_max: {}, mfi_exit_max: {}\n""".format(

ma_window_max, ma_fast_window_max, ma_slow_window_max,

macd_slow_window_max, macd_fast_window_max, macd_sign_window_max,

rsi_window_max, rsi_entry_max, rsi_exit_max,

stoch_window_max, stoch_smooth_window_max, stoch_entry_max, stoch_exit_max,

bb_window_max, bb_dev_max, mfi_window_max,

mfi_entry_max, mfi_exit_max))

print(" Now I'm doing the calculations. It may take me some time (it depends on the power of your computer)\n\

and the amount of data I have to analyze. So, be patient and relax for now.\n")

trading_signals = SuperAI_Ind.run(open_prices, high_prices, low_prices, close_prices, volume, buylesstime, selltime,

ma_window = ma_window_opt,

ma_fast_window = ma_fast_window_opt,

ma_slow_window = ma_slow_window_opt,

macd_slow_window = macd_slow_window_opt,

macd_fast_window = macd_fast_window_opt,

macd_sign_window = macd_sign_window_opt,

rsi_window = rsi_window_opt,

rsi_entry = rsi_entry_opt,

rsi_exit = rsi_exit_opt,

stoch_window = stoch_window_opt,

stoch_smooth_window = stoch_smooth_window_opt,

stoch_entry = stoch_entry_opt,

stoch_exit = stoch_exit_opt,

bb_window = bb_window_opt,

bb_dev = bb_dev_opt,

mfi_window = mfi_window_opt,

mfi_entry = mfi_entry_opt,

mfi_exit = mfi_exit_opt,

param_product = True)

entries = trading_signals.output == 1.0

exits = trading_signals.output == -1.0

SuperAI_portfolio = vbt.Portfolio.from_signals(close_prices,

entries,

exits,

init_cash = 100000,

tp_stop = take_profit_percent,

sl_stop = stop_loss_percent,

fees = 0.00)

stats_all = SuperAI_portfolio.stats()

returns = SuperAI_portfolio.total_return() * 100

max_dd = SuperAI_portfolio.max_drawdown()

sharpe_ratio = SuperAI_portfolio.sharpe_ratio(freq='m')

#APPLYING THE BEST PARAMETERS TO THE MODEL

(ma_window_max, ma_fast_window_max, ma_slow_window_max,

macd_slow_window_max, macd_fast_window_max, macd_sign_window_max,

rsi_window_max, rsi_entry_max, rsi_exit_max,

stoch_window_max, stoch_smooth_window_max, stoch_entry_max, stoch_exit_max,

bb_window_max, bb_dev_max, mfi_window_max,

mfi_entry_max, mfi_exit_max) = returns.idxmax() #max_dd.idxmax() #sharpe_ratio.idxmax()

trading_signals = SuperAI_Ind.run(open_prices, high_prices, low_prices, close_prices, volume, buylesstime, selltime,

ma_window = ma_window_max,

ma_fast_window = ma_fast_window_max,

ma_slow_window = ma_slow_window_max,

macd_slow_window = macd_slow_window_max,

macd_fast_window = macd_fast_window_max,

macd_sign_window = macd_sign_window_max,

rsi_window = rsi_window_max,

rsi_entry = rsi_entry_max,

rsi_exit= rsi_exit_max,

stoch_window = stoch_window_max,

stoch_smooth_window = stoch_smooth_window_max,

stoch_entry = stoch_entry_max,

stoch_exit = stoch_exit_max,

bb_window = bb_window_max,

bb_dev = bb_dev_max,

mfi_window = mfi_window_max,

mfi_entry = mfi_entry_max,

mfi_exit= mfi_exit_max,

param_product = True)

entries = trading_signals.output == 1.0

exits = trading_signals.output == -1.0

SuperAI_portfolio = vbt.Portfolio.from_signals(close_prices,

entries,

exits,

init_cash = 100000,

tp_stop = take_profit_percent,

sl_stop = stop_loss_percent,

fees = 0.00)

opt_returns = SuperAI_portfolio.total_return() * 100

optimized_returns = opt_returns

opt_stats = SuperAI_portfolio.stats()

print("I optimized the parameters.")

print("The parameters after optimization are:\n")

print(""" ma_window_max: {}, ma_fast_window_max: {}, ma_slow_window_max: {},

macd_slow_window_max: {}, macd_fast_window_max: {}, macd_sign_window_max: {},

rsi_window_max: {}, rsi_entry_max: {}, rsi_exit_max: {},

stoch_window_max: {}, stoch_smooth_window_max: {}, stoch_entry_max: {}, stoch_exit_max: {},

bb_window_max: {}, bb_dev_max: {},

mfi_window_max: {}, mfi_entry_max: {}, mfi_exit_max: {}\n""".format(

ma_window_max, ma_fast_window_max, ma_slow_window_max,

macd_slow_window_max, macd_fast_window_max, macd_sign_window_max,

rsi_window_max, rsi_entry_max, rsi_exit_max,

stoch_window_max, stoch_smooth_window_max, stoch_entry_max, stoch_exit_max,

bb_window_max, bb_dev_max, mfi_window_max,

mfi_entry_max, mfi_exit_max))

print("\nMax returns after optimization: ", opt_returns, "\n")

print("Stats after optimization:")

print(opt_stats, "\n")

else:

print("You declared You don't want any optimization. I respect that and I'm not going to do any optimization.\n")

#VALIDATION OF THE MODEL

if validation == True:

print("I start the validation. I'm downloading the data for {} from {} to {}.".format(asset, valid_start, valid_end))

print("For previous calculations I used data for {} from {} to {}.".format(asset, data_start, data_end))

open_prices, high_prices, low_prices, close_prices, volume, buylesstime, selltime = prepare_data(valid_start, valid_end)

print("I've got the data. I'm starting the calculations.\n")

trading_signals = SuperAI_Ind.run(open_prices, high_prices, low_prices, close_prices, volume, buylesstime, selltime,

ma_window = ma_window_max,

ma_fast_window = ma_fast_window_max,

ma_slow_window = ma_slow_window_max,

macd_slow_window = macd_slow_window_max,

macd_fast_window = macd_fast_window_max,

macd_sign_window = macd_sign_window_max,

rsi_window = rsi_window_max,

rsi_entry = rsi_entry_max,

rsi_exit= rsi_exit_max,

stoch_window = stoch_window_max,

stoch_smooth_window = stoch_smooth_window_max,

stoch_entry = stoch_entry_max,

stoch_exit = stoch_exit_max,

bb_window = bb_window_max,

bb_dev = bb_dev_max,

mfi_window = mfi_window_max,

mfi_entry = mfi_entry_max,

mfi_exit= mfi_exit_max,

param_product = True)

entries = trading_signals.output == 1.0

exits = trading_signals.output == -1.0

SuperAI_portfolio = vbt.Portfolio.from_signals(close_prices,

entries,

exits,

init_cash = 100000,

tp_stop = take_profit_percent,

sl_stop = stop_loss_percent,

fees = 0.00)

val_returns = SuperAI_portfolio.total_return() * 100

validated_returns = val_returns

val_stats = SuperAI_portfolio.stats()

print("I've finished the validation.\n")

print("Returns from validation: ", val_returns, "\n")

print("Stats from validation:")

print(val_stats, "\n")

else:

print("You declared You don't want to do any validation. Ok, I won't do any.\n")

strategy_returns[0] = cs_name

strategy_returns[1] = basic_returns

strategy_returns[2] = optimized_returns

strategy_returns[3] = validated_returns

strategy_to_df = pd.DataFrame([strategy_returns], columns=columns)

global strategies

strategies = pd.concat([strategies, strategy_to_df])

print(""" Now You have to decide whether we go with this strategy to live paper trading

or you want to try another strategy. Whatever your decision is, I'm here for you.\n\n""")

# 2. ALL THE OTHER FUNCTIONS AND VARIABLES OF THE BOT NEEDED FOR LIVE TRADING WITH PAPER TRADING ACCOUNT

#Taking profit

profit_ratio = 100 + (take_profit_percent * 100)

def take_profit(close_price, sell_order_filled):

if take_profit_automatically == True:

try:

position = api.get_position(asset)

aep = float(api.get_position(asset).avg_entry_price)

if sell_order_filled == False:

if close_price >= aep * profit_ratio / 100:

n_shares = float(position.qty)

api.submit_order(symbol=asset,qty=n_shares,side='sell',type='market',time_in_force='gtc')

print("Take profit price is {}% from {:.2f}$ we paid for 1 {} = {:.2f}$. "

.format(profit_ratio, aep, asset, aep * profit_ratio / 100))

print('The current {:.2f}$ is good enough. We take profit with an order to sell {} shares/coins of {}.'

.format(close_price, n_shares, asset))

else:

print('Take profit price is {}% from the price we used for buying: {:.2f}$ for 1 {} and that is {:.2f}$.'

.format(profit_ratio, aep, asset, aep * profit_ratio / 100))

print('Last close price {:.2f}$ is not enough.'.format(close_price))

except:

pass

print()

else:

pass

#Stopping loss

stoploss_ratio = 100 - (stop_loss_percent * 100)

def stop_loss(close_price, sell_order_filled):

if stop_loss_automatically == True:

try:

position = api.get_position(asset)

aep = float(api.get_position(asset).avg_entry_price)

if sell_order_filled == False:

if close_price < aep * stoploss_ratio / 100:

n_shares = float(position.qty)

api.submit_order(symbol=asset,qty=n_shares,side='sell',type='market',time_in_force='gtc')

print("Stop loss price is {}% from {:.2f}$ we paid for 1 {} = {:.2f}$."

.format(stoploss_ratio, aep, asset, aep * stoploss_ratio / 100))

print('The current {:.2f}$ is less. We stop loss with an order to sell {} shares/coins of {}.'

.format(close_price, n_shares, asset))

else:

print("Stop loss price is {}% from the price we used for buying: {:.2f}$ for 1 {} and that is {:.2f}$."

.format(stoploss_ratio, aep, asset, aep * stoploss_ratio / 100))

print("Last close price {:.2f}$ is not that low.".format(close_price))

except:

pass

print()

else:

pass

# Caclulating Technical Indicators and Candlestick Patterns Signals

def cal_tech_ind(open_prices, high_prices, low_prices, close_prices, volume, buylesstime, selltime):

#CALCULATING TECHNICAL INDICATORS SIGNALS

close_price = close_prices[-1]

#Calculating MA Signals

try:

ma = ta.trend.ema_indicator(close_prices, window = ma_window_max)

ma = np.round(ma, 2)

ma_last = float(ma.iloc[-1])

ma_fast = ta.trend.ema_indicator(close_prices, window = ma_fast_window_max)

ma_fast = np.round(ma_fast, 2)

ma_fast_last = float(ma_fast.iloc[-1])

ma_slow = ta.trend.ema_indicator(close_prices, window = ma_slow_window_max)

ma_slow = np.round(ma_slow, 2)

ma_slow_last = float(ma_slow.iloc[-1])

print("Last MA is: {:.3f}. Last Fast MA is: {:.3f}. Last Slow MA is: {:.3f}.\n".format(ma_last,

ma_fast_last, ma_slow_last))

except:

print ("MA signal doesn't work.\n")

#Calculating MACD Signal

try:

macd = ta.trend.macd(close_prices, window_slow = macd_slow_window_max, window_fast = macd_fast_window_max)

macd = np.round(macd, 2)

macd_last = float(macd.iloc[-1])

macd_diff = ta.trend.macd_diff(close_prices, window_slow = macd_slow_window_max,

window_fast = macd_fast_window_max, window_sign = macd_sign_window_max)

macd_diff = np.round(macd_diff, 2)

macd_diff_last = float(macd_diff.iloc[-1])

macd_sign = ta.trend.macd_signal(close_prices, window_slow = macd_slow_window_max,

window_fast = macd_fast_window_max, window_sign = macd_sign_window_max)

macd_sign = np.round(macd_sign, 2)

macd_sign_last = float(macd_sign.iloc[-1])

print("Last MACD is: {:.3f}. Last MACD_DIFF is: {:.3f}. Last MACD_SIGNAL is: {:.3f}.\n".format(macd_last,

macd_diff_last, macd_sign_last))

except:

print ("MACD signal doesn't work.\n")

#Calculating RSI Signal

try:

rsi = ta.momentum.rsi(close_prices, window = rsi_window_max)

rsi = np.round(rsi, 2)

rsi_last = rsi.iloc[-1]

rsi_entry = rsi_entry_max

rsi_exit = rsi_exit_max

print("Last RSI is {:.3f}. RSI thresholds are: {:.2f} - {:.2f}.\n".format(rsi_last, rsi_entry, rsi_exit))

except:

print("RSI signal doesn't work.\n")

#Calculating Stochastic Signal

try:

stoch = ta.momentum.stoch(high_prices, low_prices, close_prices,

window = stoch_window_max, smooth_window = stoch_smooth_window_max)

stoch = np.round(stoch, 2)

stoch_last = stoch.iloc[-1]

stoch_sign = ta.momentum.stoch_signal(high_prices, low_prices, close_prices,

window = stoch_window_max, smooth_window = stoch_smooth_window_max)

stoch = np.round(stoch_sign, 2)

stoch_sign_last = stoch_sign.iloc[-1]

stoch_entry = stoch_entry_max

stoch_exit = stoch_exit_max

print("Last Stochastic is {:.3f}. Stochastic thresholds are: {:.2f} - {:.2f}.\n".format(

stoch_last, stoch_entry, stoch_exit))

print("Last Stochastic Signal is {:.3f}. Stochastic thresholds are: {:.2f} - {:.2f}.\n".format(

stoch_sign_last, stoch_entry, stoch_exit))

except:

print("Stochastic signal doesn't work.\n")

#Calculating Bollinger Bands Signal

try:

bb_low = ta.volatility.bollinger_lband(close_prices, window=bb_window_max, window_dev = bb_dev_max)

bb_low = np.round(bb_low, 2)

bb_high = ta.volatility.bollinger_hband(close_prices, window=bb_window_max, window_dev = bb_dev_max)

bb_high = np.round(bb_high, 2)

bb_low_last = float(bb_low.iloc[-1])

bb_high_last = float(bb_high.iloc[-1])

print("Last price is: {}$. Bollinger Bands are: Lower: {:.3f}, Upper: {:.3f}.\n".format(close_price,

bb_low_last, bb_high_last))

except:

print ("Bollinger Bands signal doesn't work.\n")

#Calculating MFI Signal

try:

mfi = ta.volume.money_flow_index(high_prices, low_prices, close_prices, volume, window = mfi_window_max)

mfi = np.round(mfi, 2)

mfi_last = mfi.iloc[-1]

mfi_entry = mfi_entry_max

mfi_exit = mfi_exit_max

print("Last MFI is {:.3f}. MFI thresholds are: {:.2f} - {:.2f}.\n".format(mfi_last, mfi_entry, mfi_exit))

except:

print("MFI signal doesn't work.\n")

return (ma, ma_fast, ma_slow,

macd, macd_diff, macd_sign,

rsi, rsi_entry, rsi_exit,

stoch, stoch_sign, stoch_entry, stoch_exit,

bb_low, bb_high,

mfi, mfi_entry, mfi_exit)

#SuperAI Trading Bot

def cal_can_pat(open_prices, high_prices, low_prices, close_prices, volume, buylesstime, selltime):

#CALCULATING CANDLESTICK PATTERNS AND SIGNALS

#Hammer

candle_buy_signal_1 = ta_lib.CDLHAMMER(open_prices, high_prices, low_prices, close_prices)

last_candle_buy_signal_1 = candle_buy_signal_1.iloc[-1]

print("Last Candle Buy Signal 1: {}.".format(last_candle_buy_signal_1))

#Morning Star

candle_buy_signal_2 = ta_lib.CDLMORNINGSTAR(open_prices, high_prices, low_prices, close_prices)

last_candle_buy_signal_2 = candle_buy_signal_2.iloc[-1]

print("Last Candle Buy Signal 2: {}.".format(last_candle_buy_signal_2))

#Three White Soldiers

candle_buy_signal_3 = ta_lib.CDL3WHITESOLDIERS(open_prices, high_prices, low_prices, close_prices)

last_candle_buy_signal_3 = candle_buy_signal_3.iloc[-1]

print("Last Candle Buy Signal 3: {}.".format(last_candle_buy_signal_3))

#Shooting Star

candle_sell_signal_1 = ta_lib.CDLSHOOTINGSTAR(open_prices, high_prices, low_prices, close_prices)

last_candle_sell_signal_1 = candle_sell_signal_1.iloc[-1]

print("Last Candle Sell Signal 1: {}.".format(last_candle_sell_signal_1))

#Evening Star

candle_sell_signal_2 = ta_lib.CDLEVENINGSTAR(open_prices, high_prices, low_prices, close_prices)

last_candle_sell_signal_2 = candle_sell_signal_2.iloc[-1]

print("Last Candle Sell Signal 2: {}.".format(last_candle_sell_signal_2))

#3 Black Crows

candle_sell_signal_3 = ta_lib.CDL3BLACKCROWS(open_prices, high_prices, low_prices, close_prices)

last_candle_sell_signal_3 = candle_sell_signal_3.iloc[-1]

print("Last Candle Sell Signal 3: {}.".format(last_candle_sell_signal_3))

#Engulfing (Bullish (buy) / Bearish (Sell))

candle_buy_sell_signal_1 = ta_lib.CDLENGULFING(open_prices, high_prices, low_prices, close_prices)

last_candle_buy_sell_signal_1 = candle_buy_sell_signal_1.iloc[-1]

print("Last Candle Buy Sell Signal 1: {}.".format(last_candle_buy_sell_signal_1))

#Three Outside: Up (buy) / Down (sell)

candle_buy_sell_signal_2 = ta_lib.CDL3OUTSIDE(open_prices, high_prices, low_prices, close_prices)

last_candle_buy_sell_signal_2 = candle_buy_sell_signal_2.iloc[-1]

print("Last Candle Buy Sell Signal 2: {}.".format(last_candle_buy_sell_signal_2))

return (candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3,

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3,

candle_buy_sell_signal_1, candle_buy_sell_signal_2)

# Check if market is open

def check_if_market_open():

if api.get_clock().is_open == False:

print("The market is closed at the moment.")

print("Time to open is around: {:.0f} minutes. So I'll stop working for now. Hope you don't mind."

.format((api.get_clock().next_open.timestamp()- api.get_clock().timestamp.timestamp())/60))

sys.exit("I'm out. Turn me back on when it's time. Yours, SuperAI trader.")

else:

pass

#Buyless time

def buyless_time(time_now):

(trading_hour_start, trading_hour_stop,

buyless_time_start_1, buyless_time_end_1, buyless_time_start_2, buyless_time_end_2,

selltime_start, selltime_end) = trading_buy_sell_time()

buyless1_start = datetime.time(int(buyless_time_start_1[:2]), int(buyless_time_start_1[3:]))

buyless1_end = datetime.time(int(buyless_time_end_1[:2]), int(buyless_time_end_1[3:]))

buyless2_start = datetime.time(int(buyless_time_start_2[:2]), int(buyless_time_start_2[3:]))

buyless2_end = datetime.time(int(buyless_time_end_2[:2]), int(buyless_time_end_2[3:]))

buylesstime = (buyless1_start < time_now < buyless1_end) | (buyless2_start < time_now < buyless2_end)

print('is it buyless time? ', buylesstime)

return buylesstime

#Sell time

def sell_time(time_now):

(trading_hour_start, trading_hour_stop,

buyless_time_start_1, buyless_time_end_1, buyless_time_start_2, buyless_time_end_2,

selltime_start, selltime_end) = trading_buy_sell_time()

sell_time_start = datetime.time(int(selltime_start[:2]), int(selltime_start[3:]))

sell_time_end = datetime.time(int(selltime_end[:2]), int(selltime_end[3:]))

selltime = (sell_time_start < time_now < sell_time_end)

print('is it sell time? ', selltime)

return selltime

#Waiting for a bar to close

#check for more: https://alpaca.markets/learn/code-cryptocurrency-live-trading-bot-python-alpaca/

def wait_for_bar_to_close():

time_now = datetime.datetime.now()

next_min = time_now.replace(second=5, microsecond=0) + timedelta(minutes=1)

pause = math.ceil((next_min - time_now).seconds)

print("I'll wait {} seconds for the bar to close.".format(pause))

print("\n* * * * * * * * * * * * * * * * * * * * * * * * *\n")

return pause

# Function to run after starting the bot (on_open function)

def on_open():

print("\nI'm connected to Alpaca API and ready to work. I'm starting to watch the prices.\n")

cash = float(api.get_account().cash)

print("We have {:.2f}$ cash.".format(cash))

try:

position = api.get_position(asset)

n_shares = float(position.qty)

print("We have {} shares/coins of {}.\n".format(n_shares, asset))

except:

print("We don't have any shares/coins of {} at the moment.\n".format(asset))

funds = cash * funds_percentage / 100

print("Funds we will use for trading: {:.2f}$.\n".format(funds))

print("I will be trading {}.\n".format(asset))

try:

print("The last backtest I did was for {}.\n".format(backtested_asset))

except:

print("I didn't do any backtesting yet.\n")

global trading_hour_start, trading_hour_stop

global buyless_time_start_1, buyless_time_end_1, buyless_time_start_2, buyless_time_end_2

global selltime_start, selltime_end

(trading_hour_start, trading_hour_stop,

buyless_time_start_1, buyless_time_end_1, buyless_time_start_2, buyless_time_end_2,

selltime_start, selltime_end) = trading_buy_sell_time()

print(""" I will be trading between {} and {}.

I won't be buying between {} and {} and between {} and {}.

I will sell the shares/coins of {} when it's between {} and {} no matter the trading signals.\n""".format(

trading_hour_start, trading_hour_stop,

buyless_time_start_1, buyless_time_end_1, buyless_time_start_2, buyless_time_end_2, asset,

selltime_start, selltime_end, "\n"))

if take_profit_automatically:

print("Take profit is set to +{}% from the average entry price.".format(take_profit_percent*100))

print("I will be trading when the technical indicators and candlestick patterns say so, but also")

print("if entry price is e.g. 100$ I'll automatically sell when last close price is more than 100$+{}%*100$={:.2f}$"

.format(take_profit_percent * 100, 100*profit_ratio/100))

else:

print("Take profit automatically is turned off.")

print("I will use technical indicators and candlestick patterns to get as much profit as I can.")

if stop_loss_automatically:

print("\nStop loss is set to -{}% from the average entry price.".format(stop_loss_percent*100))

print("I will be trading when the technical indicators and candlestick patterns say so, but also")

print("if entry price is e.g. 100$ I'll automatically sell when last close price is less than 100$-{}%*100$={:.2f}$"

.format(stop_loss_percent * 100, 100*stoploss_ratio/100))

else:

print("\nStop loss automatically is turned off.")

print("I will use technical indicators and candlestick patterns so I don't lose money.")

print("\nSo, here we go. Wish me luck.\n")

print("* * * * * * * * * * * * * * * * * * * * * * * * *\n")

if asset_type == "stock":

check_if_market_open()

# Function to run after every message from Alpaca (on_message function)

def on_message():

nyc_datetime = api.get_clock().timestamp.tz_convert('America/New_York')

print("New York time:", str(nyc_datetime)[:16])

open_prices, high_prices, low_prices, close_prices, volume, buylesstime, selltime = prepare_data(

str(datetime.date.today() - datetime.timedelta(days = 2)),

str(datetime.date.today() + datetime.timedelta(days = 2)))

close_price = close_prices[-1]

print("Close price of {}: {:.2f}$\n".format(asset, close_price))

try:

position = api.get_position(asset)

n_shares = float(position.qty)

print("We have {} shares/coins of {}.\n".format(n_shares, asset))

except:

print("We don't have any shares/coins of {} at the moment.\n".format(asset))

cash = float(api.get_account().cash)

print("We have {:.2f}$ cash.".format(cash))

funds = cash * funds_percentage / 100

print("Funds we will use for trading: {:.2f}$.\n".format(funds))

#CALCULATING TECHNICAL INDICATORS SIGNALS

(ma, ma_fast, ma_slow, macd, macd_diff, macd_sign, rsi, rsi_entry, rsi_exit,

stoch, stoch_sign, stoch_entry, stoch_exit,

bb_low, bb_high, mfi, mfi_entry, mfi_exit) = cal_tech_ind(

open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime)

#CALCULATING CANDLESTICK PATTERNS AND SIGNALS

(candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3,

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3,

candle_buy_sell_signal_1, candle_buy_sell_signal_2) = cal_can_pat(

open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime)

#Calculate final trade signal

try:

final_trade_signals = create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime,

ma, ma_fast, ma_slow,

macd, macd_diff, macd_sign,

rsi, rsi_entry, rsi_exit,

stoch, stoch_sign, stoch_entry, stoch_exit,

bb_low, bb_high,

mfi, mfi_entry, mfi_exit,

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3,

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3,

candle_buy_sell_signal_1, candle_buy_sell_signal_2)

final_trade_signal = final_trade_signals[-1]

if final_trade_signal == 0:

print("\nFinal trade signal is: DO NOTHING\n")

elif final_trade_signal == 1:

print("\nFinal trade signal is: BUY\n")

elif final_trade_signal == -1:

print("\nFinal trade signal is: SELL\n")

except:

print("\nFinal trade signal doesn't work.\n")

final_trade_signal = False

#Execute action after recieving the final trade signal: submitting an order

sell_order_filled = False

if final_trade_signal == 1: #"buy":

try:

api.get_position(asset)

print("We hit the threshold to buy, but we already have some shares/coins, so we won't buy more.\n")

except:

n_shares = np.round(funds // close_price)

if asset_type == 'crypto':

#an overcomplicated way to round down the number of coins to buy to the declared number of places after comma

n_shares = funds//close_price + float((str((funds / close_price)-(funds//close_price))[:(2+rounding)]))

api.submit_order(symbol=asset,qty=n_shares,side="buy",type="market",time_in_force="gtc")

print('We submitted the order to buy {} {} shares/coins.'.format(n_shares, asset))

try:

position = api.get_position(asset)

aep = float(api.get_position(asset).avg_entry_price)

print("The last close price was {}. We bought {} shares/coins of {} for the price of: {}$ for 1 {}.\n".format(

close_price, n_shares, asset, aep, asset))

except:

pass

elif final_trade_signal == -1: #"sell":

try:

position = api.get_position(asset)

n_shares = float(position.qty)

api.submit_order(symbol=asset,qty=n_shares,side='sell',type='market',time_in_force='gtc')

sell_order_filled = True

print('We submitted an order to sell {} {} shares/coins.'.format(n_shares, asset))

except:

print("We hit the threshold to sell, but we don't have anything to sell. Next time maybe.\n")

else:

print("The signal was inconclusive - probably indicators showed us we should wait, so we wait.\n")

#Hand-made take profit

take_profit(close_price, sell_order_filled)

#Hand-made stop loss

stop_loss(close_price, sell_order_filled)

print("\n* * * * * * * * * * * * * * * * * * * * * * * * *\n")

if asset_type == "stock":

check_if_market_open()

# Function to run the bot until break or until the market is closed

def SuperAI_Trading_Bot():

on_open()

time.sleep(wait_for_bar_to_close())

while True:

on_message()

time.sleep(wait_for_bar_to_close())

print("You've interrupted me. That's it than. I hope I did good. Till the next time.")

And now we have all we need. Now we can run the bot.

So, here we go!

#SuperAI Trading Bot - optional cell

#the asset was declared at the beginning of the program, but you can change it here if you want

#(asset, asset_type, rounding) = ("BTCUSD", "crypto", 0)

#(asset, asset_type, data_source) = ("AAPL", "stock", "Yahoo")

SuperAI_Backtester()

If you want to trade crypto, you have to choose one that Alpaca supports at the moment: https://alpaca.markets/support/what-cryptocurrencies-does-alpaca-currently-support/

You should also check the minimum quantity you can trade.

If you want to trade stocks you may choose ticker of the company you prefer: https://www.nyse.com/listings_directory/stock

Your data_source can be 'Alpaca' or 'Yahoo', just know that:

#SuperAI Trading Bot - 7. mandatory cell to run

#the asset was declared at the beginning of the program, but you can change it here if you want

#(asset, asset_type, rounding) = ("BTCUSD", "crypto", 0)

#(asset, asset_type, data_source) = ("AAPL", "stock", "Yahoo")

SuperAI_Trading_Bot()

And that's it. Now we can start testing different strategies.

* '>' here represents the crossing over

* '<' here represents the crossing under

#SuperAI Trading Bot - optional cell

# the same variables that were previously declared, copied here for convenience,

# so we don't have to go to the beginning of the program every time we want to change them

(asset, asset_type, data_source) = ("AAPL", "stock", "Yahoo")

#(asset, asset_type, rounding) = ("BTCUSD", "crypto", 0)

optimization = False

validation = True

(data_start, data_end) = ('2022-07-01', '2022-07-31')

(valid_start, valid_end) = ('2022-08-01', '2022-08-15')

#SuperAI Trading Bot - optional cell

#DataFrame for testing various strategies

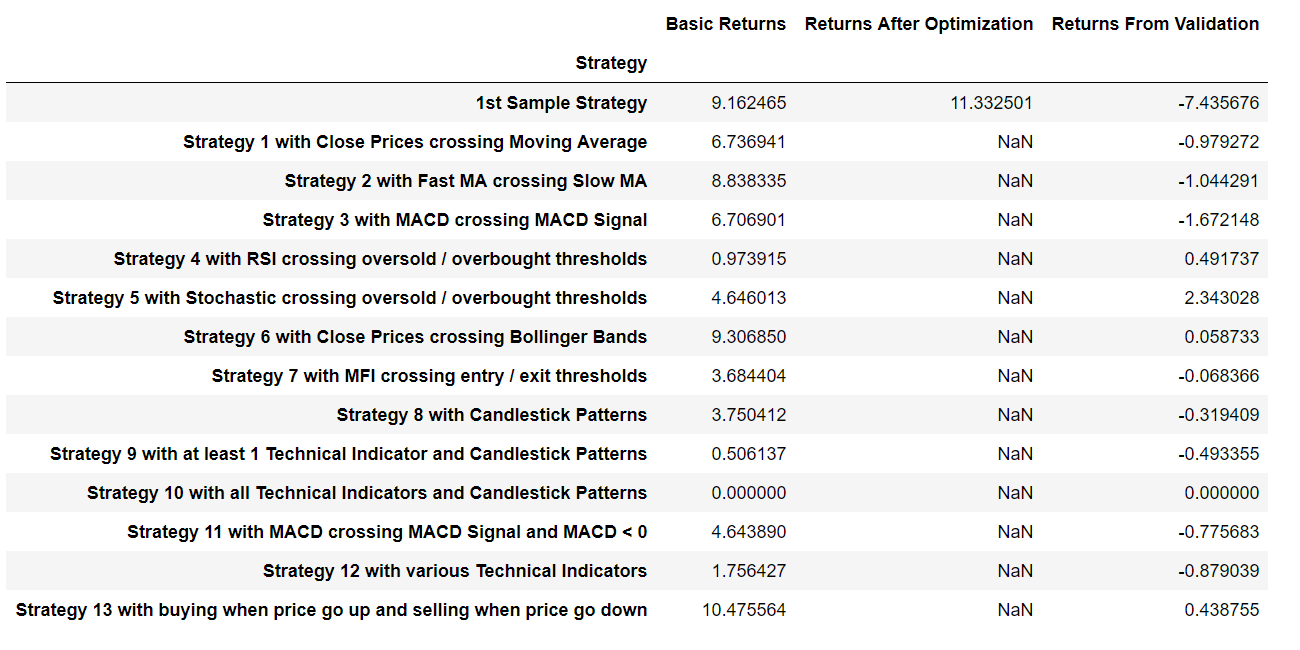

strategies

#SuperAI Trading Bot - optional cell

# 1. STRATEGY

# BUY when CLOSE PRICE crosses over MA ==> SELL when CLOSE PRICE crosses under MA

def create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime, #Time to abstain from buying and forced selling

ma, ma_fast, ma_slow, #Moving Average

macd, macd_diff, macd_sign, #Moving Average Convergence Divergence

rsi, rsi_entry, rsi_exit, #Relative Strength Index

stoch, stoch_signal, stoch_entry, stoch_exit, #Stochastic

bb_low, bb_high, #Bollinger Bands

mfi, mfi_entry, mfi_exit, #Money Flow Index

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3, #Candle signals to buy

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3, #Candle signals to sell

candle_buy_sell_signal_1, candle_buy_sell_signal_2): #Candle signals to buy or sell

SuperAI_signal_buy = np.where(

(buylesstime != 1)

&

((close_prices > ma) & (shifted(close_prices, 1) <= shifted(ma, 1)))

, 1, 0) #1 is buy, -1 is sell, 0 is do nothing

SuperAI_signal = np.where(

(selltime == 1)

|

((close_prices < ma) & (shifted(close_prices, 1) >= shifted(ma, 1)))

, -1, SuperAI_signal_buy) #1 is buy, -1 is sell, 0 is do nothing

global cs_name

cs_name = 'Strategy 1 with Close Prices crossing Moving Average'

return SuperAI_signal

#SuperAI Trading Bot - optional cell

SuperAI_Backtester()

#SuperAI Trading Bot - optional cell

# 2. STRATEGY

# BUY when FAST MA crosses over SLOW MA ==> SELL when FAST MA crosses under SLOW MA

def create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime, #Time to abstain from buying and forced selling

ma, ma_fast, ma_slow, #Moving Average

macd, macd_diff, macd_sign, #Moving Average Convergence Divergence

rsi, rsi_entry, rsi_exit, #Relative Strength Index

stoch, stoch_signal, stoch_entry, stoch_exit, #Stochastic

bb_low, bb_high, #Bollinger Bands

mfi, mfi_entry, mfi_exit, #Money Flow Index

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3, #Candle signals to buy

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3, #Candle signals to sell

candle_buy_sell_signal_1, candle_buy_sell_signal_2): #Candle signals to buy or sell

SuperAI_signal_buy = np.where(

(buylesstime != 1)

&

((ma_fast > ma_slow) & (shifted(ma_fast, 1) <= shifted(ma_slow, 1)))

, 1, 0) #1 is buy, -1 is sell, 0 is do nothing

SuperAI_signal = np.where(

(selltime == 1)

|

((ma_fast < ma_slow) & (shifted(ma_fast, 1) >= shifted(ma_slow, 1)))

, -1, SuperAI_signal_buy) #1 is buy, -1 is sell, 0 is do nothing

global cs_name

cs_name = 'Strategy 2 with Fast MA crossing Slow MA'

return SuperAI_signal

#SuperAI Trading Bot - optional cell

SuperAI_Backtester()

#SuperAI Trading Bot - optional cell

# 3. STRATEGY

# BUY when MACD crosses over MACD SIGNAL ==> SELL when MACD crosses under MACD SIGNAL

def create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime, #Time to abstain from buying and forced selling

ma, ma_fast, ma_slow, #Moving Average

macd, macd_diff, macd_sign, #Moving Average Convergence Divergence

rsi, rsi_entry, rsi_exit, #Relative Strength Index

stoch, stoch_signal, stoch_entry, stoch_exit, #Stochastic

bb_low, bb_high, #Bollinger Bands

mfi, mfi_entry, mfi_exit, #Money Flow Index

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3, #Candle signals to buy

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3, #Candle signals to sell

candle_buy_sell_signal_1, candle_buy_sell_signal_2): #Candle signals to buy or sell

SuperAI_signal_buy = np.where(

(buylesstime != 1)

&

((macd > macd_sign) & (shifted(macd, 1) <= shifted(macd_sign, 1)))

, 1, 0) #1 is buy, -1 is sell, 0 is do nothing

SuperAI_signal = np.where(

(selltime == 1)

|

((macd < macd_sign) & (shifted(macd, 1) >= shifted(macd_sign, 1)))

, -1, SuperAI_signal_buy) #1 is buy, -1 is sell, 0 is do nothing

global cs_name

cs_name = 'Strategy 3 with MACD crossing MACD Signal'

return SuperAI_signal

#SuperAI Trading Bot - optional cell

SuperAI_Backtester()

#SuperAI Trading Bot - optional cell

# 4. STRATEGY

# BUY when RSI crosses under RSI OVERSOLD THRESHOLD ==> SELL when RSI crosses over RSI OVERBOUGHT THRESHOLD

def create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime, #Time to abstain from buying and forced selling

ma, ma_fast, ma_slow, #Moving Average

macd, macd_diff, macd_sign, #Moving Average Convergence Divergence

rsi, rsi_entry, rsi_exit, #Relative Strength Index

stoch, stoch_signal, stoch_entry, stoch_exit, #Stochastic

bb_low, bb_high, #Bollinger Bands

mfi, mfi_entry, mfi_exit, #Money Flow Index

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3, #Candle signals to buy

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3, #Candle signals to sell

candle_buy_sell_signal_1, candle_buy_sell_signal_2): #Candle signals to buy or sell

SuperAI_signal_buy = np.where(

(buylesstime != 1)

&

((rsi < rsi_entry) & (shifted(rsi, 1) >= rsi_entry))

, 1, 0) #1 is buy, -1 is sell, 0 is do nothing

SuperAI_signal = np.where(

(selltime == 1)

|

((rsi > rsi_exit) & (shifted(rsi, 1) <= rsi_exit))

, -1, SuperAI_signal_buy) #1 is buy, -1 is sell, 0 is do nothing

global cs_name

cs_name = 'Strategy 4 with RSI crossing oversold / overbought thresholds'

return SuperAI_signal

#SuperAI Trading Bot - optional cell

SuperAI_Backtester()

#SuperAI Trading Bot - optional cell

# 5. STRATEGY

# BUY when STOCHASTIC crosses under STOCHASTIC OVERSOLD THRESHOLD

# ==> SELL when STOCHASTIC crosses over STOCHASTIC OVERBOUGHT THRESHOLD

def create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime, #Time to abstain from buying and forced selling

ma, ma_fast, ma_slow, #Moving Average

macd, macd_diff, macd_sign, #Moving Average Convergence Divergence

rsi, rsi_entry, rsi_exit, #Relative Strength Index

stoch, stoch_signal, stoch_entry, stoch_exit, #Stochastic

bb_low, bb_high, #Bollinger Bands

mfi, mfi_entry, mfi_exit, #Money Flow Index

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3, #Candle signals to buy

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3, #Candle signals to sell

candle_buy_sell_signal_1, candle_buy_sell_signal_2): #Candle signals to buy or sell

SuperAI_signal_buy = np.where(

(buylesstime != 1)

&

((stoch < stoch_entry) & (shifted(stoch, 1) >= stoch_entry))

, 1, 0) #1 is buy, -1 is sell, 0 is do nothing

SuperAI_signal = np.where(

(selltime == 1)

|

((stoch > stoch_exit) & (shifted(stoch, 1) <= stoch_exit))

, -1, SuperAI_signal_buy) #1 is buy, -1 is sell, 0 is do nothing

global cs_name

cs_name = 'Strategy 5 with Stochastic crossing oversold / overbought thresholds'

return SuperAI_signal

#SuperAI Trading Bot - optional cell

SuperAI_Backtester()

#SuperAI Trading Bot - optional cell

# 6. STRATEGY

# BUY when CLOSE PRICE crosses under LOWER BOLLINGER BAND ==> SELL when CLOSE PRICE crosses over HIGHER BOLLINGER BAND

def create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime, #Time to abstain from buying and forced selling

ma, ma_fast, ma_slow, #Moving Average

macd, macd_diff, macd_sign, #Moving Average Convergence Divergence

rsi, rsi_entry, rsi_exit, #Relative Strength Index

stoch, stoch_signal, stoch_entry, stoch_exit, #Stochastic

bb_low, bb_high, #Bollinger Bands

mfi, mfi_entry, mfi_exit, #Money Flow Index

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3, #Candle signals to buy

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3, #Candle signals to sell

candle_buy_sell_signal_1, candle_buy_sell_signal_2): #Candle signals to buy or sell

SuperAI_signal_buy = np.where(

(buylesstime != 1)

&

((close_prices < bb_low) & (shifted(close_prices, 1) >= shifted(bb_low, 1)))

, 1, 0) #1 is buy, -1 is sell, 0 is do nothing

SuperAI_signal = np.where(

(selltime == 1)

|

((close_prices > bb_high) & (shifted(close_prices, 1) <= shifted(bb_high, 1)))

, -1, SuperAI_signal_buy) #1 is buy, -1 is sell, 0 is do nothing

global cs_name

cs_name = 'Strategy 6 with Close Prices crossing Bollinger Bands'

return SuperAI_signal

#SuperAI Trading Bot - optional cell

SuperAI_Backtester()

#SuperAI Trading Bot - optional cell

# 7. STRATEGY

# BUY when MFI crosses under MFI ENTRY THRESHOLD ==> SELL when MFI crosses over MFI EXIT THRESHOLD

def create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime, #Time to abstain from buying and forced selling

ma, ma_fast, ma_slow, #Moving Average

macd, macd_diff, macd_sign, #Moving Average Convergence Divergence

rsi, rsi_entry, rsi_exit, #Relative Strength Index

stoch, stoch_signal, stoch_entry, stoch_exit, #Stochastic

bb_low, bb_high, #Bollinger Bands

mfi, mfi_entry, mfi_exit, #Money Flow Index

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3, #Candle signals to buy

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3, #Candle signals to sell

candle_buy_sell_signal_1, candle_buy_sell_signal_2): #Candle signals to buy or sell

SuperAI_signal_buy = np.where(

(buylesstime != 1)

&

((mfi < mfi_entry) & (shifted(mfi, 1) >= mfi_entry))

, 1, 0) #1 is buy, -1 is sell, 0 is do nothing

SuperAI_signal = np.where(

(selltime == 1)

|

((mfi > mfi_exit) & (shifted(mfi, 1) <= mfi_exit))

, -1, SuperAI_signal_buy) #1 is buy, -1 is sell, 0 is do nothing

global cs_name

cs_name = 'Strategy 7 with MFI crossing entry / exit thresholds'

return SuperAI_signal

#SuperAI Trading Bot - optional cell

SuperAI_Backtester()

#SuperAI Trading Bot - optional cell

# 8. STRATEGY

# BUY when at least 1 of 5 CANDLESTICK PATTERNS shows to BUY ==> SELL when at least 1 of 5 CANDLESTICK PATTERNS shows to SELL

def create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime, #Time to abstain from buying and forced selling

ma, ma_fast, ma_slow, #Moving Average

macd, macd_diff, macd_sign, #Moving Average Convergence Divergence

rsi, rsi_entry, rsi_exit, #Relative Strength Index

stoch, stoch_signal, stoch_entry, stoch_exit, #Stochastic

bb_low, bb_high, #Bollinger Bands

mfi, mfi_entry, mfi_exit, #Money Flow Index

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3, #Candle signals to buy

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3, #Candle signals to sell

candle_buy_sell_signal_1, candle_buy_sell_signal_2): #Candle signals to buy or sell

SuperAI_signal_buy = np.where(

(buylesstime != 1)

&

((candle_buy_signal_1 > 0) | (candle_buy_signal_2 > 0) | (candle_buy_signal_3 > 0)

| (candle_buy_sell_signal_1 > 0) | (candle_buy_sell_signal_2 > 0))

, 1, 0) #1 is buy, -1 is sell, 0 is do nothing

SuperAI_signal = np.where(

(selltime == 1)

|

((candle_sell_signal_1 < 0) | (candle_sell_signal_2 < 0) | (candle_buy_signal_3 < 0)

| (candle_buy_sell_signal_1 < 0) | (candle_buy_sell_signal_2 < 0))

, -1, SuperAI_signal_buy) #1 is buy, -1 is sell, 0 is do nothing

global cs_name

cs_name = 'Strategy 8 with Candlestick Patterns'

return SuperAI_signal

#SuperAI Trading Bot - optional cell

SuperAI_Backtester()

* '>' here represents the crossing over

* '<' here represents the crossing under

#SuperAI Trading Bot - optional cell

# 9. STRATEGY

# BUY when 1 of 7 TECHNICAL INDICATORS shows to BUY (CP > MA or FAST MA > SLOW MA or MACD > MACD SIGNAL or RSI > RSI ENTRY

# or STOCHASTIC > STOCHASTIC ENTRY or CP < BB LOW or MFI > MFI ENTRY)* AND 1 of 5 CANDLESTICK PATTERNS shows to BUY

# ==> SELL when 1 of 7 TECHNICAL INDICATORS shows to SELL (CP < MA or FAST MA < SLOW MA or MACD < MACD SIGNAL or RSI > RSI EXIT

# or STOCHASTIC > STOCHASTIC EXIT or CP > BB HIGH or MFI > MFI EXIT)* or 1 of 7 CANDLESTICK PATTERNS shows to SELL

def create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime, #Time to abstain from buying and forced selling

ma, ma_fast, ma_slow, #Moving Average

macd, macd_diff, macd_sign, #Moving Average Convergence Divergence

rsi, rsi_entry, rsi_exit, #Relative Strength Index

stoch, stoch_signal, stoch_entry, stoch_exit, #Stochastic

bb_low, bb_high, #Bollinger Bands

mfi, mfi_entry, mfi_exit, #Money Flow Index

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3, #Candle signals to buy

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3, #Candle signals to sell

candle_buy_sell_signal_1, candle_buy_sell_signal_2): #Candle signals to buy or sell

SuperAI_signal_buy = np.where(

(buylesstime != 1)

&

(

(

((close_prices > ma) & (shifted(close_prices, 1) <= shifted(ma, 1)))

|

((ma_fast > ma_slow) & (shifted(ma_fast, 1) <= shifted(ma_slow, 1)))

|

((macd > macd_sign) & (shifted(macd, 1) <= shifted(macd_sign, 1)))

|

((rsi < rsi_entry) & (shifted(rsi, 1) >= rsi_entry))

|

((stoch < stoch_entry) & (shifted(stoch, 1) >= stoch_entry))

|

((close_prices < bb_low) & (shifted(close_prices, 1) >= shifted(bb_low, 1)))

|

((mfi < mfi_entry) & (shifted(mfi, 1) >= mfi_entry))

)

&

((candle_buy_signal_1 > 0) | (candle_buy_signal_2 > 0) | (candle_buy_signal_3 > 0)

| (candle_buy_sell_signal_1 > 0) | (candle_buy_sell_signal_2 > 0))

)

, 1, 0) #1 is buy, -1 is sell, 0 is do nothing

SuperAI_signal = np.where(

(selltime == 1)

|

(

((close_prices < ma) & (shifted(close_prices, 1) >= shifted(ma, 1)))

|

((ma_fast < ma_slow) & (shifted(ma_fast, 1) >= shifted(ma_slow, 1)))

|

((macd < macd_sign) & (shifted(macd, 1) >= shifted(macd_sign, 1)))

|

((rsi > rsi_exit) & (shifted(rsi, 1) <= rsi_exit))

|

((stoch > stoch_exit) & (shifted(stoch, 1) <= stoch_exit))

|

((close_prices > bb_high) & (shifted(close_prices, 1) <= shifted(bb_high, 1)))

|

((mfi > mfi_exit) & (shifted(mfi, 1) <= mfi_exit))

)

|

((candle_sell_signal_1 < 0) | (candle_sell_signal_2 < 0) | (candle_buy_signal_3 < 0)

| (candle_buy_sell_signal_1 < 0) | (candle_buy_sell_signal_2 < 0))

, -1, SuperAI_signal_buy) #1 is buy, -1 is sell, 0 is do nothing

global cs_name

cs_name = 'Strategy 9 with at least 1 Technical Indicator and Candlestick Patterns'

return SuperAI_signal

#SuperAI Trading Bot - optional cell

SuperAI_Backtester()

* '>' here represents the crossing over

* '<' here represents the crossing under

#SuperAI Trading Bot - optional cell

# 10. STRATEGY

# BUY when ALL 7 TECHNICAL INDICATORS show to BUY (CP > MA and FAST MA > SLOW MA and MACD > MACD SIGNAL and RSI > RSI ENTRY

# and STOCHASTIC > STOCHASTIC ENTRY and CP < BB LOW, and MFI > MFI ENTRY)* AND 1 of 5 CANDLESTICK PATTERNS shows to BUY

# ==> SELL when 1 of 7 TECHNICAL INDICATORS shows to SELL (CP < MA or FAST MA < SLOW MA or MACD < MACD SIGNAL or RSI > RSI EXIT

# or STOCHASTIC > STOCHASTIC EXIT or CP > BB HIGH or MFI > MFI EXIT)* or 1 of 7 CANDLESTICK PATTERNS shows to SELL

def create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime, #Time to abstain from buying and forced selling

ma, ma_fast, ma_slow, #Moving Average

macd, macd_diff, macd_sign, #Moving Average Convergence Divergence

rsi, rsi_entry, rsi_exit, #Relative Strength Index

stoch, stoch_signal, stoch_entry, stoch_exit, #Stochastic

bb_low, bb_high, #Bollinger Bands

mfi, mfi_entry, mfi_exit, #Money Flow Index

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3, #Candle signals to buy

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3, #Candle signals to sell

candle_buy_sell_signal_1, candle_buy_sell_signal_2): #Candle signals to buy or sell

SuperAI_signal_buy = np.where(

(buylesstime != 1)

&

(

(

((close_prices > ma) & (shifted(close_prices, 1) <= shifted(ma, 1)))

&

((ma_fast > ma_slow) & (shifted(ma_fast, 1) <= shifted(ma_slow, 1)))

&

((macd > macd_sign) & (shifted(macd, 1) <= shifted(macd_sign, 1)))

&

((rsi < rsi_entry) & (shifted(rsi, 1) >= rsi_entry))

&

((stoch < stoch_entry) & (shifted(stoch, 1) >= stoch_entry))

&

((close_prices < bb_low) & (shifted(close_prices, 1) >= shifted(bb_low, 1)))

&

((mfi < mfi_entry) & (shifted(mfi, 1) >= mfi_entry))

)

&

((candle_buy_signal_1 > 0) | (candle_buy_signal_2 > 0) | (candle_buy_signal_3 > 0)

| (candle_buy_sell_signal_1 > 0) | (candle_buy_sell_signal_2 > 0))

)

, 1, 0) #1 is buy, -1 is sell, 0 is do nothing

SuperAI_signal = np.where(

(selltime == 1)

|

(

((close_prices < ma) & (shifted(close_prices, 1) >= shifted(ma, 1)))

|

((ma_fast < ma_slow) & (shifted(ma_fast, 1) >= shifted(ma_slow, 1)))

|

((macd < macd_sign) & (shifted(macd, 1) >= shifted(macd_sign, 1)))

|

((rsi > rsi_exit) & (shifted(rsi, 1) <= rsi_exit))

|

((stoch > stoch_exit) & (shifted(stoch, 1) <= stoch_exit))

|

((close_prices > bb_high) & (shifted(close_prices, 1) <= shifted(bb_high, 1)))

|

((mfi > mfi_exit) & (shifted(mfi, 1) <= mfi_exit))

)

|

((candle_sell_signal_1 < 0) | (candle_sell_signal_2 < 0) | (candle_buy_signal_3 < 0)

| (candle_buy_sell_signal_1 < 0) | (candle_buy_sell_signal_2 < 0))

, -1, SuperAI_signal_buy) #1 is buy, -1 is sell, 0 is do nothing

global cs_name

cs_name = 'Strategy 10 with all Technical Indicators and Candlestick Patterns'

return SuperAI_signal

#SuperAI Trading Bot - optional cell

SuperAI_Backtester()

#SuperAI Trading Bot - optional cell

# 11. STRATEGY

# BUY when MACD crosses over MACD SIGNAL only when MACD < 0 ==> SELL when MACD crosses under MACD SIGNAL

def create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime, #Time to abstain from buying and forced selling

ma, ma_fast, ma_slow, #Moving Average

macd, macd_diff, macd_sign, #Moving Average Convergence Divergence

rsi, rsi_entry, rsi_exit, #Relative Strength Index

stoch, stoch_signal, stoch_entry, stoch_exit, #Stochastic

bb_low, bb_high, #Bollinger Bands

mfi, mfi_entry, mfi_exit, #Money Flow Index

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3, #Candle signals to buy

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3, #Candle signals to sell

candle_buy_sell_signal_1, candle_buy_sell_signal_2): #Candle signals to buy or sell

SuperAI_signal_buy = np.where(

(buylesstime != 1)

&

((macd < 0) & (macd > macd_sign) & (shifted(macd, 1) <= shifted(macd_sign, 1)))

, 1, 0) #1 is buy, -1 is sell, 0 is do nothing

SuperAI_signal = np.where(

(selltime == 1)

|

((macd < macd_sign) & (shifted(macd, 1) >= shifted(macd_sign, 1)))

, -1, SuperAI_signal_buy) #1 is buy, -1 is sell, 0 is do nothing

global cs_name

cs_name = 'Strategy 11 with MACD crossing MACD Signal and MACD < 0'

return SuperAI_signal

#SuperAI Trading Bot - optional cell

SuperAI_Backtester()

#SuperAI Trading Bot - optional cell

# 12. STRATEGY (from previous tutorial)

# BUY when MACD crosses over MACD SIGNAL only when MACD < 0 and (MA is higher than MA from 2 minutes before

# and MA from 2 minutes before is higher than MA from 4 minutes before)

# ==> SELL when (STOCHASTIC is over STOCHASTIC EXIT and RSI over RSI EXIT) or (CP over BB HIGH and MFI over MFI EXIT)

def create_signal(open_prices, high_prices, low_prices, close_prices, volume,

buylesstime, selltime, #Time to abstain from buying and forced selling

ma, ma_fast, ma_slow, #Moving Average

macd, macd_diff, macd_sign, #Moving Average Convergence Divergence

rsi, rsi_entry, rsi_exit, #Relative Strength Index

stoch, stoch_signal, stoch_entry, stoch_exit, #Stochastic

bb_low, bb_high, #Bollinger Bands

mfi, mfi_entry, mfi_exit, #Money Flow Index

candle_buy_signal_1, candle_buy_signal_2, candle_buy_signal_3, #Candle signals to buy

candle_sell_signal_1, candle_sell_signal_2, candle_sell_signal_3, #Candle signals to sell